Setting up a virtual bank in Thailand

5 March 2024 marks an important milestone for the Thai financial sector, as the Bank of Thailand (“BOT”) announced that a notification regarding applications for virtual bank licences in Thailand has been published in the Royal Gazette, and come into effect on 20 March 2024. The BOT believes that introduction of virtual banks as new key players will redefine the financial landscape and help steer the Thai financial sector toward a sustainable digital economy. This also represents an attempt to provide Thai customers with financial services and innovations similar to those already available in many other jurisdictions, including the United Kingdom, Singapore, South Korea, Taiwan, Hong Kong, Malaysia, and Australia.

1 Introduction

In this newsletter, we will discuss key issues and details related to setting up a virtual bank in Thailand pursuant to the Ministry of Finance’s Notification Re: Rules, Procedures, and Conditions for the Application for and Issuance of a Virtual Bank Licence dated 20 February 2024 (the “Virtual Bank Licence Notification”) as well as the BOT’s Consultation Paper on Virtual Banks, published in June 2023 (the “Virtual Bank Consultation Paper”).

It is worth noting that the development of a framework for virtual banks is still at an early stage. Thus, any information provided by the BOT in the Virtual Bank Consultation Paper may be subject to further changes. Also, it is expected that the Ministry of Finance will publish additional notifications regarding the regulatory framework for virtual banks, and that subsequent BOT notifications and public handbooks on virtual banks also will be published at a later stage. Therefore, updates on this matter should be monitored closely.

The primary topics covered in this newsletter are:

- 1) Licensing framework for setting up virtual banks; and

- 2) Virtual bank application and selection processes.

2 Licensing framework for setting up virtual banks

1. Key qualifications for virtual bank applicants

The following table lists the key qualifications required of virtual bank applicants, pursuant to the Virtual Bank Licence Notification and the Virtual Bank Consultation Paper.

|

Qualification |

Details |

|---|---|

|

1. Sustainable Business Model |

The applicant needs to clearly demonstrate the capability to operate a virtual bank, in keeping with the proposed business model and business plan, and to provide credible reasoning. At a minimum, the proposed business plan must demonstrate the applicant’s ability to:

|

|

2. Robust Governance |

Qualifications related to governance include:

|

|

3. Adequate Digital Service Expertise |

The IT plan for the proposed virtual bank needs to be clear and suitable to the business model, particularly in terms of IT governance, IT architecture, and IT personnel. In addition, virtual banks must not share critical IT systems, such as core banking, mobile banking, and internet banking systems, with other financial institutions. The IT risk management standards should be in accordance with BOT notifications and subject to assessment by an external IT expert. |

|

4. Adequate Technology and IT Systems |

|

|

5. Capacity to Manage Financial Business Risks |

The risk management plan must demonstrate the capacity to manage financial business risks. Also, the applicant should demonstrate that it has:

|

|

6. Ability to Access, Manage, and Utilise Diverse Types of Data |

The operational plan for data must be clear, realistic, and suited to the business. |

|

7. Robust Financial Position |

Virtual bank applicants must demonstrate appropriate financial capabilities, sources of capital, and liquidity, including a clear and credible plan for capital increases, as well as a commitment to provide adequate funding and oversight for the virtual bank. |

- 2. Business scope and service channel

The Virtual Bank Consultation Paper mentions the following principles as key business scope and service channels for virtual banks:- Virtual banks shall be incorporated locally, in Thailand, as public companies limited, with initial paid-up capital of not less than THB 5 billion1, and may provide full-service banking business, albeit without physical branches. Thus, they will be able to serve all groups of customers, in a manner similar to traditional commercial banks.

- Virtual banks need to operate and serve customers principally through digital channels. They are prohibited from establishing physical and electronic branches, including automated teller machines (ATMs) and cash deposit machines (CDMs).

- Virtual banks must establish a local headquarters in Thailand2 for purposes of effective BOT supervision and examinations, as well as for customer contacts and complaints when necessary.

3 Virtual bank application and selection processes

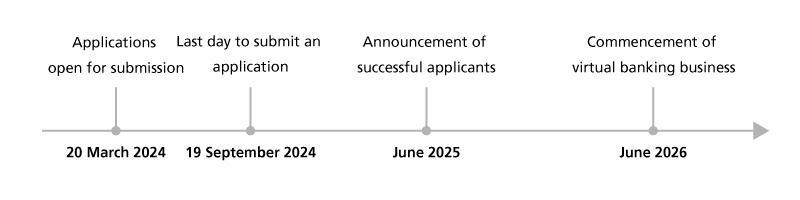

Applications for virtual bank licences will open in limited rounds, and will open only from 20 March 2024 until

19 September 20243. Thereafter, the BOT will begin reviewing all applications and preparing a list of the most appropriate candidates for consideration by the Minister of Finance. The review processes should take no longer than 9 months, in total.4

In the initial stage, the BOT expects to include no more than 3 candidates on the list to be submitted to the Minister of Finance. The reason is that an excessive number of new players may pose risks to the stability of the financial system and the financial institution system. In particular, the retail loan market already has a high level of competition.

It is expected that successful applicants will be announced during the second quarter of 2025. These successful applicants then must undertake various preparatory actions, including establishment and review of IT systems and risk management tools, to commence virtual bank operations within 1 year from the date of approval.

The following is a tentative timeline for the next steps in relevant processes.

Jirapong Sriwat

Partner

Apinya Sarntikasem

Partner

Korntawat Jiraruangrattana

Associate

1Clause 8 of the Virtual Bank Licence Notification

2Clause 8 of the Virtual Bank Licence Notification

3Pursuant to Clause 1 and 5 of the Virtual Bank Licence Notification

4The review processes could be extended by up to 1 year pursuant to Clause 8 of the Virtual Bank Licence Notification

Authors

Apinya’s extensive practice covers a wide array of matters ranging from business set-up, domestic and cross-border transactions to day-to-day business operations, to name a few. Her clientele includes both local and international conglomerates, trading companies, aircraft operators, real estate developers, petroleum and energy companies, financial institutions, securities companies, venture capitalists, and fund managers. Well-read and a holder of law degrees from three different jurisdictions - Thailand, the United States and Japan, Apinya is able to leverage her international experience and cultural insights to effectively and efficiently resolve complex cross-border legal issues and provide tailored legal services and solutions to her clients. In addition to being a practicing lawyer, Apinya is regularly invited to teach business law at various prestigious universities in Thailand, and serves as a counsellor to the Ad-hoc Committee of the House of Representatives of Thailand for consideration of amendments to the Civil and Commercial Code. Her other notable achievements include being registered as a Barrister-at-Law, Attorney-at-Law, and Notarial Services Attorney in Thailand.

Related Knowledge

-

New DBD Capital Verification Requirements

Articles

-

-

Thailand’s Latest Move to Facilitate Foreign Direct Investment: Proposal to Delist 10 Restricted Businesses Under the Foreign Business Act

Articles

- Jirapong SRIWAT

- Apinya SARNTIKASEM

- Panthakant LIN and others

-

-

Preparing for the Future Tax Impact of Climate Change

Articles

-

-

Bank of Thailand Relaxes Foreign Exchange Controls to Support Private Sector Transactions

Articles

-

-

Sustainability Management for Increasing Corporate Value over the Mid- to Long-term and Roles of Audit & Supervisory Board Members

External Seminars

-

-

Thailand Employment Laws for Expats and Executives

Online

External Seminars

He advises on a wide range of merger-and-acquisition transactions, joint ventures, foreign direct investments, general corporate, international corporate finance, and restructurings. His expertise is advising, structuring and leading complex transactions both within and outside of Thailand. He regularly represents, among others, Japanese, Thai and international investors, international investment banks, international private equity investors, hedge funds and international corporations and financial institutions. His main areas of practice include public and private mergers and acquisitions (takeover rules), legal due diligence, joint ventures, fund raising, listings, block trades, stock exchange and securities exchange related laws, restructuring of shareholdings and general corporate advice. His additional areas of practice also cover banking and finance, renewable energy in Japan and Thailand, exchange control law, labor law, and debt restructurings. Before setting up the Bangkok office of Nishimura & Asahi in 2013, he worked with Linklaters for almost a decade. He is also a registered arbitrator of the Thai Arbitration Institute (TAI) with the areas of expertise in corporate M&A, joint venture, banking and finance, capital markets, debt restructurings and energy.